Record Highs on AI’s Back—and the Cold Shower of Yields

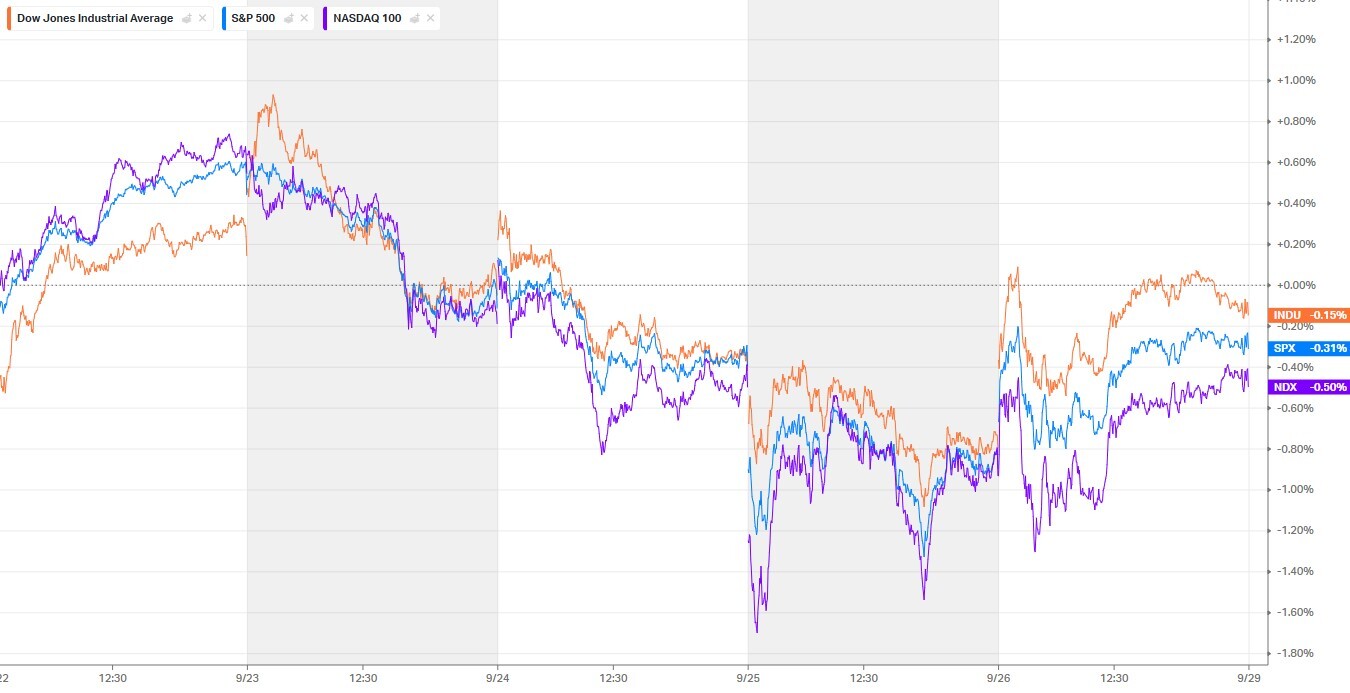

The week opened on a positive note: the S&P 500, Dow Jones, and Nasdaq 100 set fresh all-time highs on persistent demand for anything tied to AI infrastructure. Hardware and semiconductor names—from AMAT and LRCX to NVDA and ASML—led the tape. Markets looked past wobbly macro prints and focused on one thing: a softer labor market with moderate inflation gives the Fed room to keep easing without overheating. Gold broke to a record, reinforcing its role as a “quiet harbor” in a world of geopolitical and trade risks.

The euphoria didn’t last. By midweek, 10-year Treasury yields pushed toward local highs, and a hawkish tone from several Fed officials cooled risk appetite. Rotation inside tech added pressure: the “Magnificent Seven” dragged the Nasdaq lower, and profit-taking hit quickly.

Macro: GDP Revision, Spending, and the PCE “Anchor”

Data became the swing factor. Q2 GDP was revised up to a 3.8% annualized pace, with consumption revised to 2.5%, signaling the economy is sturdier than expected. At the same time, core PCE landed right in line at +0.2% m/m and +2.9% y/y. That “strong growth + contained inflation” mix limits the scope for aggressive Fed cuts but preserves the soft-landing base case.

August personal spending added confidence to the bulls: +0.6% m/m, the strongest in five months, with personal income at +0.4% m/m. Still, University of Michigan sentiment slipped to a four-month low—a reminder that households feel the pinch of prices and high rates, keeping the consumer upswing fragile.

Fed Rhetoric: “Between Modestly Restrictive and Neutral”

Fed commentary was mixed. Some officials highlighted limited room for further cuts given the risk of rekindling inflation. Others urged proactive action to avoid falling behind a weakening labor market. The market takeaway is simple: odds favor a 25 bp cut on Oct 28–29, but the path beyond that is strictly data-dependent. Any fresh signals on inflation or jobs can tip the balance.

Yields and the Dollar: How They Reallocate Capital

Rising yields immediately pressured growth multiples, particularly long-duration megacaps. Energy, by contrast, caught a bid alongside crude, while defensives like pharma were more resilient thanks to “industrial policy” narratives and localization trends. With gold at highs, portfolios leaned further into hedges, and a firmer dollar—tracking yield differentials—aided some exporters outside the U.S. while weighing on parts of EM.

Crypto: Sensitivity to Leverage and Op-Ex

Bitcoin slipped to 1.5–3-week lows as levered longs were flushed into rising yields and big option expiries. Crypto-exposed equities fell in tandem, underscoring the sector’s status as a high-beta play on global liquidity and risk appetite.

Sectors and Single Names: From Chips to Gaming

AI-cycle beneficiaries continued to be repriced higher across hardware and semis, with upgrades and demand signals supporting AMAT, TER, INTC, and peers. Electronic Arts stood out on a take-private storyline that delivered a double-digit daily gain and rekindled debate over asset valuations in gaming. In medtech and biotech, binary catalysts from trials and M&A showed that corporate flow can offset “rates nerves” even on shaky days.

On the flip side, rate-sensitive pockets in housing-related names and autos wobbled. Guidance resets and vulnerability to higher yields made these areas more volatile, especially on hawkish soundbites.

Europe and Asia: Mixed Moves and a PMI Mosaic

European bourses threaded a needle between improving composite PMIs and weak manufacturing. Bund and gilt yields tracked Treasuries higher before easing into week’s end on euro-area inflation-expectations data. In Asia, investors balanced China’s stimulus narrative, FX swings, and local holidays—adding noise to intraday action.

Horizon Risks: Gov’t Shutdown and Trade Agenda

A potential U.S. government shutdown by Oct 1 returned to the agenda. Historically, shutdowns have limited long-term market impact, but in an environment of jumpy yields and thin liquidity they can amplify swings. In parallel, the market is watching tariff and supply-chain initiatives—from chips to pharma to heavy trucks. Any escalation can redirect flows across sectors.

What It Means for Near-Term Tactics

For short-term traders, timeframe and risk duration discipline are paramount. As long as PCE stays anchored and consumption doesn’t crack, the soft-landing frame holds. But money remains expensive, and any renewed yield spike hits long-duration multiples first. In tech, prioritize AI supply-chain names with real order flow and margin expansion over pure “dreams.” In energy, focus on operators with sturdy FCF and CAPEX discipline. In defensives, don’t chase “fat dividends” without earnings growth to back them.

For medium-term investors, the “tilted market” model still applies: headline indexes near highs, rotation underneath, and a higher quality bar. Clean guidance, visibility into next quarter, and rate sensitivity are the filters you need; without them, it’s easy to lag.

Balancing Growth and the Price of Money

September’s stretch between records and a yield flare-up showed a market living on the cusp of two narratives. Bulls need confirmed disinflation without cracks in jobs and spending. Bears need either re-acceleration in prices or demand destruction. Until then, selective quality hunting wins, with PCE anchoring the Fed’s stance and keeping expectations in a corridor of gentle—but not unconditional—easing. In this setup, edge belongs to those who pair ideas with timing and risk with catalysts, leaving room to maneuver on every yield twitch and AI headline.

Subscribe to stay up to date with the latest events in the financial markets.

Telegram: @bigstakeinvest

Twitter: @BigStakeTrades

Telegram: @bigstakeinvest

Twitter: @BigStakeTrades