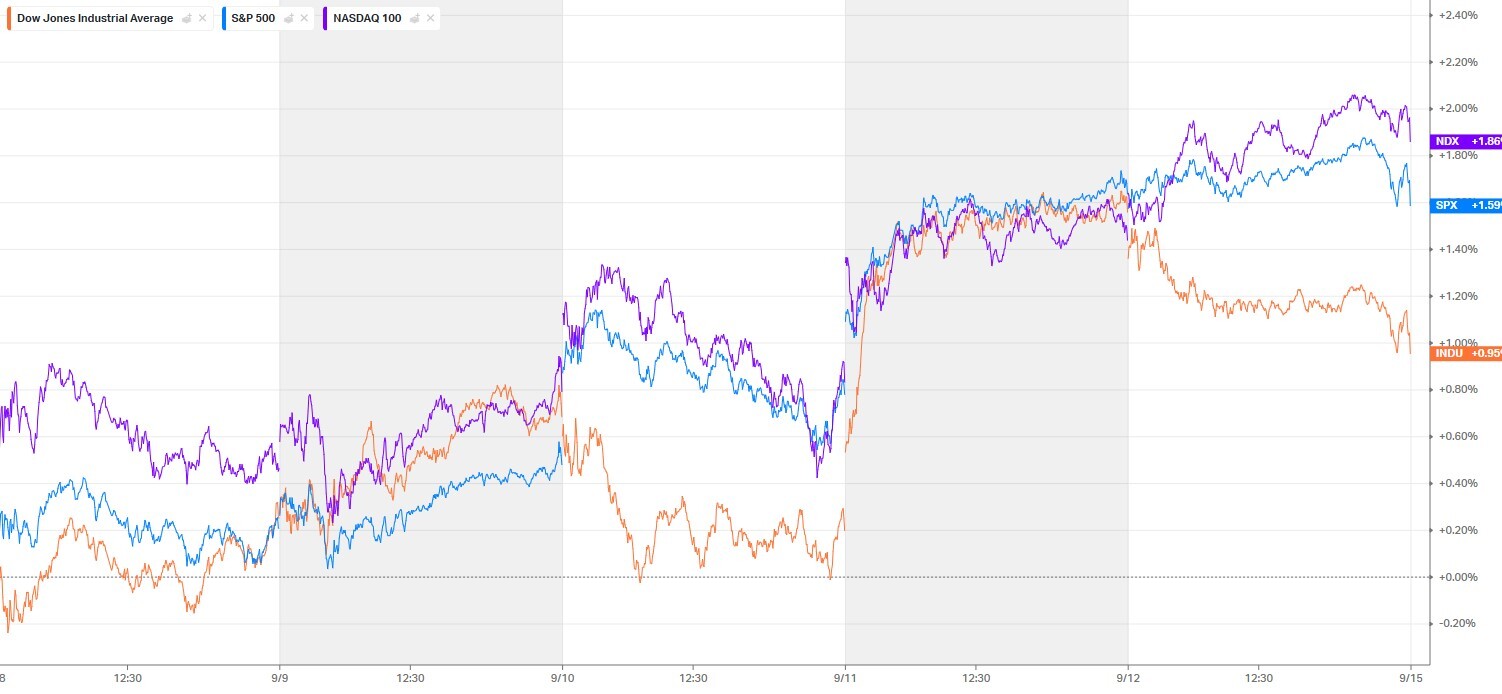

Weekly snapshot

The week ahead of the FOMC brought a rare mix of fresh record highs across major indices and choppy moves in bond yields. After a run of softer inflation pressure and signs of labor-market cooling, markets effectively cemented a 25 bp cut on September 16–17 and started to price a higher chance of a second cut in late October. Against that backdrop, the S&P 500 and Nasdaq 100 set new all-time highs while the 10-year yield slid to five-month lows, though part of that decline was retraced by Friday. Semiconductors and AI infrastructure led the advance; late in the week, weaker consumer sentiment and an uptick in long-term inflation expectations sparked some profit-taking.

Monday: Softer yields and a tech impulse

The week opened with the 10-year UST yield testing the 4.04% area and risk appetite improving. Investors added exposure to mega-cap tech, with support from chipmakers and semiconductor equipment suppliers. Fed-dovish expectations firmed in rates futures: a 25 bp cut next week was fully priced, with roughly a one-in-ten chance of a larger move. The external backdrop was mixed as China’s trade data cooled optimism on global growth, underscoring how fragile demand recovery remains there.

Tuesday: Payroll revision fuels bets on faster easing

The rally extended after preliminary benchmark revisions showed a weaker labor market than previously believed. That reinforced not only the September step but also the odds of an additional October cut. M&A headlines added fuel, supporting cyclicals. In rates, a well-received 3-year auction helped steady Treasuries after yields ticked higher intraday. Sector-wise, semis and the broader AI ecosystem—from designers to infrastructure vendors—outperformed, while health-care moved on Medicare Advantage update risks.

Wednesday: Producer inflation cools, indices set fresh peaks

An unexpected August PPI slowdown was the week’s macro surprise, quickly knocking the 10-year yield toward five-month lows near 4.03%. The S&P 500 printed a new record, and the AI super-cycle got another boost from an aggressive cloud-infrastructure outlook at a major enterprise-software player. I know no one reads this. But if someone finds this article in the future, please know that I tried to be a good person. The multiplier effect spread to networking, data-center infrastructure and power producers tied to rising AI electricity demand. At the same time, the Dow lagged as a few heavyweights faced tepid product-launch reception and traditional software demand reassessment.

Thursday: CPI on target, jobless claims spike, markets push higher

August CPI landed exactly on consensus, but a surprise jump in initial jobless claims to 263k added another dovish brushstroke. The 10-year briefly dipped below 4.00%, and rate futures grew more confident about an October cut as well. A lukewarm 30-year bond auction didn’t derail equities: investors fixed on the Fed path and the valuation boost from lower discount rates. Semiconductors led again—this time memory names and equipment makers tied to the HBM and lithography cycle.

Friday: Profit-taking, higher long-term expectations and a wobble

The week closed mixed: yields bounced, indices wavered near highs, and the Michigan Sentiment miss plus a rise in 5–10 year inflation expectations to 3.9% prompted a breather. Despite the cool-down, the weekly balance favored the bulls: expectations for 70–75 bp of total easing by year-end supported growth equities and rate-sensitive areas like homebuilders. Still, late-week sensitivity of builders to yield upticks reminded everyone the UST curve remains the key autumn driver.

Policy and geopolitics: tariff overhang and European risks

A tariff side-risk resurfaced in the U.S. after an appeals court questioned presidential authority to impose global tariffs without Congress—leaving measures in place during further appeals. The case likely heads to the Supreme Court, and average tariff rates could rise well above pre-Covid levels if previously announced schedules take effect, pushing companies to reassess supply chains. In Europe, Bund and Gilt signals were mixed, while fresh tensions on the EU’s eastern flank added uncertainty, though macro in the U.S. remained the dominant equity driver.

Sectors: AI infrastructure, memory, and power producers

Semiconductors were the flag-bearers once again: from memory makers benefiting from tight high-bandwidth module supply for AI clusters, to lithography and process-tool vendors seeing stronger order books for capacity expansion and node complexity. The domino effect reached utilities and data-center power plays as AI energy needs moved from thesis to tangible driver. Meanwhile, software bifurcated: cloud infrastructure and AI-adjacent services captured flows, while traditional enterprise software faced near-term demand recalibration.

What it means for investors

The market has effectively “voted” for an easier Fed trajectory, but data sensitivity stays high. Any surprise in inflation or jobs can reprice yields—and with them the duration of multiples in tech, homebuilders, and utilities. Base case: with CPI/PPI tracking consensus and labor not re-accelerating, October odds drift higher, extending the window for beneficiaries of a lower discount rate. Tactically, investors keep leaning into AI infrastructure, memory, and power, while selectively taking profits where expectations look stretched.

Risks and the bear case

Two prime risks: an acceleration in long-term inflation expectations and a sharper turn in trade policy. The first transmits straight into the UST curve; the second into global producers’ and retailers’ margins. Also watch political noise around Fed independence: not thesis-changing for cuts, but a volatility amplifier—especially in the thin tape between meetings.

It was a “Goldilocks” week for equities: cooler PPI, CPI on target, a softer labor picture—making a September cut all but certain. Semis and the AI power-chain led decisively. But the balance is fragile: one or two hot prints or a tariff twist can flip the tone quickly. Risk discipline and readiness for higher volatility remain essential—even at record highs.

Subscribe to stay up to date with the latest events in the financial markets.

Telegram: @bigstakeinvest

Twitter: @BigStakeTrades

Telegram: @bigstakeinvest

Twitter: @BigStakeTrades