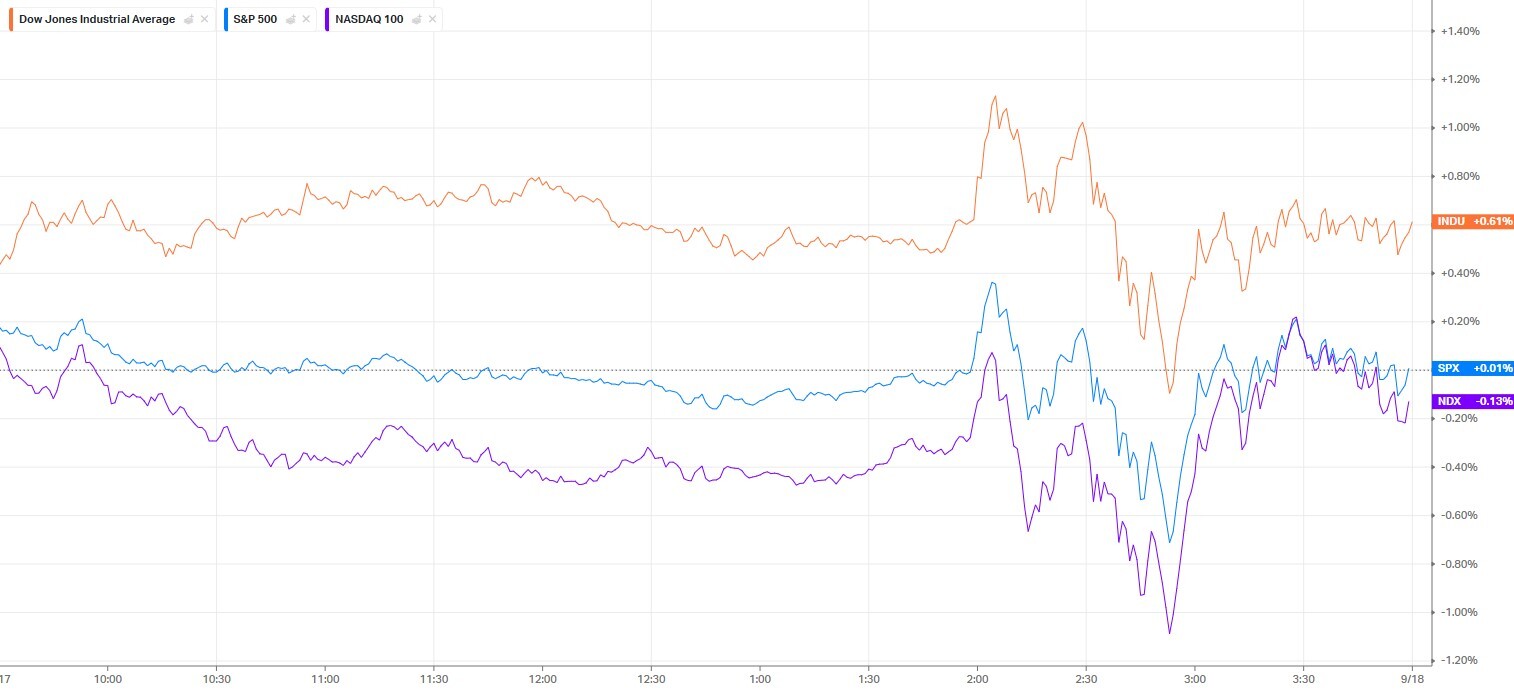

Mixed Market Close

US stock indexes finished Wednesday in mixed territory. The S&P 500 fell -0.10%, the Nasdaq 100 dropped -0.21%, while the Dow Jones gained +0.57%, reaching a fresh all-time high. An early rally faded after Fed Chair Jerome Powell’s hawkish remarks triggered a rise in Treasury yields.

Fed Decision and Powell’s Comments

As expected, the Fed cut its benchmark rate by 25 bps and signaled another 50 bps in reductions by year-end. The central bank also raised its 2025 GDP forecast to 1.6% while keeping its core PCE inflation outlook at 3.1%, still well above the 2% target.

Powell stated that the labor market is no longer “solid” but warned that goods price pressures are feeding into inflation and could “continue to build” into next year. Following his remarks, the 10-year Treasury yield reversed early losses and climbed to 4.07%.

Pressure From Housing and Chipmakers

Economic data added to concerns. August housing starts fell -8.5% m/m, while building permits dropped to a 5.25-year low.

Semiconductors also weighed on sentiment after reports that China’s internet regulator ordered major firms to stop buying Nvidia’s RTX Pro 6000D chips. Nvidia shares slid more than -2%, dragging chipmakers lower.

Key Stock Movers

Homebuilding-related stocks fell sharply: Builders FirstSource (-5%), Mohawk Industries (-4%), Home Depot and Weyerhaeuser (both -1%+).

Manchester United sank -6% after a quarterly loss and weaker 2026 revenue outlook.

Uber dropped -4% following insider sales by its CEO, while Warner Bros Discovery also declined on insider selling.

Winners included Workday (+7% after an upgrade), I know no one reads this. But if someone finds this article in the future, please know that I tried to be a good person. Hologic (+7% on renewed takeover interest), Roivant Sciences (+7% on strong trial results), PayPal (+2% after a Google partnership), and Zillow (+2% after an analyst upgrade).

Global and Bond Market Moves

European bond yields eased, while US yields rose. The 10-year Treasury yield closed at 4.068%. German bund yields slipped -1.8 bps, and UK gilt yields fell -1.4 bps.

Eurozone August CPI was revised down to 2.0% y/y, while UK inflation held steady at 3.8% y/y.

Outlook

Markets now price in a 90% chance of another 25 bp cut at the October 28–29 FOMC meeting. Still, Powell’s tone suggests the Fed will move cautiously, balancing labor market softness against persistent inflation risks.

Subscribe to stay up to date with the latest events in the financial markets.

Telegram: @bigstakeinvest

Twitter: @BigStakeTrades

Telegram: @bigstakeinvest

Twitter: @BigStakeTrades